What’s Actually Causing Your Customers to Leave?

Let’s be honest, most businesses are looking at the wrong clues when it comes to figuring out why customers leave. I’ve seen it time and time again – companies focus on surface-level churn reports that don’t tell the whole story. It’s like trying to diagnose an illness based on a single symptom. You need to dig deeper to find the real cause.

Uncovering the Hidden Culprits

Think of your payment processor logs as a hidden treasure trove. They often reveal a wealth of information about failed transactions you might not even be aware of. These failed payments are a major contributor to involuntary churn, even if the customer is happy with your service. Similarly, support tickets can shed light on recurring technical issues that are driving customers crazy. We’ve all been there – a buggy app that makes you want to throw your phone across the room. Your customers feel the same frustration. Finally, don’t underestimate the power of user behavior patterns. Things like decreased login frequency or less engagement with key features can be early warning signs of impending churn.

Beyond the Surface: The Real Churn Predictors

Your current churn metrics might be giving you a false sense of security. If you’re only looking at voluntary cancellations, you’re missing a big piece of the puzzle. A significant chunk of customer loss is due to involuntary churn. For example, in the telecommunications industry, the average churn rate can be as high as 31%. This underscores the importance of addressing potential problems before they drive customers away. This isn’t just a telecom issue; it applies to all subscription businesses. Discover more insights on churn rates across different industries.

To truly understand involuntary churn, you need to look at the right data. Instead of relying solely on exit surveys (which are useless for involuntarily churned customers), analyze payment failure reasons, track support ticket trends, and monitor in-app user engagement. These data points are much better predictors of future churn than lagging indicators like cancellation reasons. For more on digital strategy and brand building, check out the Softriver Blog. Thinking proactively shifts your focus from reactive damage control to proactive customer retention.

Identifying the Weak Points in Your System

Involuntary churn is often a symptom of problems within your own systems, not necessarily customer dissatisfaction. Imagine a leaky bucket: you can keep adding new customers, but if your payment processes are flawed, you’ll constantly lose revenue. Are your retry schedules optimized? Are your dunning emails clear and helpful, or do they sound like robotic payment demands? Are you making it easy for customers to update their payment information? These seemingly minor details can have a huge impact on your bottom line. By fixing these internal weaknesses, you can plug the leaks and hold onto more of your hard-earned revenue.

To help illustrate the common causes of involuntary churn, let’s take a look at the following table:

Common Involuntary Churn Triggers by Industry

| Industry | Primary Churn Trigger | Secondary Cause | Average Impact Rate |

|---|---|---|---|

| SaaS | Failed Payments | Expired Credit Cards | 40-50% |

| Streaming Services | Payment Declines | Insufficient Funds | 20-30% |

| Membership Sites | Billing Issues | Technical Problems | 15-20% |

| E-commerce Subscriptions | Credit Card Expiration | Customer Not Updating Information | 30-40% |

This table highlights some of the key drivers of involuntary churn across different subscription models. As you can see, failed payments and credit card issues are consistently major contributors. By understanding these trends, you can start to identify areas for improvement within your own business. Addressing these issues head-on can significantly reduce involuntary churn and boost your bottom line.

Building Payment Recovery Systems That Don’t Annoy Customers

Let’s talk about recovering failed payments without alienating your customers. I’ve seen how the most successful companies handle this – they treat each failed payment like a detective case, not a chance to spam inboxes. They’re strategic, not simply sending out generic emails and hoping for a miracle.

The Psychology of Smart Retries

The secret? Not all declined payments are the same. An expired card is a totally different beast than insufficient funds, which is different again from a bank putting a temporary hold on things. Intelligent retry sequences are key here. They adapt to the situation. Imagine a card declined due to insufficient funds. Retry it immediately? Probably not. But scheduling another attempt in a few days, maybe after payday, is much smarter.

This gives your customer breathing room to fix the issue on their end without feeling harassed. You’re maximizing your chances of recovering the payment without annoying them in the process.

Crafting Dunning Communications That Convert

Dunning, or communicating about overdue payments, shouldn’t be a negative experience. Think of it as a chance to strengthen your customer relationships. Your email subject line is your first (and maybe only) impression. Ditch the generic “Payment Failed” and try something more personal and helpful. Think along the lines of “Update Your Payment Info to Keep Accessing [Your Service]”. See the difference?

Timing is also crucial. A barrage of emails hours after a failed payment feels pushy. Spread out your communication, and tailor the message to the reason for the decline. Treat it as a customer service opportunity, not a debt collection. Instead of “Your payment failed,” try “We noticed there was a problem with your recent payment. How can we help?” It’s a small change, but it has a huge impact. Involuntary churn is often linked to things outside the customer’s control – like payment issues or technical glitches. Interestingly, media and professional services have remarkably high customer retention – around 84% in 2025. Discover more insights on customer retention rates.

Proactive Strategies: Preventing Churn Before It Happens

The best way to deal with involuntary churn? Stop it before it starts. Proactive payment updating is your friend. Features like automatic card updates through your payment processor (Stripe is a popular one) can catch issues before they become problems. Many gateways let customers store multiple payment methods, offering a backup if the primary one fails and preventing service interruptions. Even just reminding customers to update their info a few weeks before expiry can make a big difference.

The Power of Personalization

Personalizing your communications based on the customer’s history can boost recovery rates even further. A loyal, long-term subscriber might appreciate a grace period or a temporary discount if they hit a temporary snag. It shows you value them and reinforces your relationship. By blending smart retries with personalized, empathetic communication, you can turn a potentially negative situation into a chance to build trust and loyalty.

Getting Your Timing Right for Maximum Recovery Success

The difference between saving a customer and losing them can often come down to timing. I’ve seen firsthand how small adjustments to retry schedules can make a huge difference – sometimes even doubling payment recovery rates. That initial 24-hour window after a failed payment is absolutely critical, but giving up after just a week? That’s practically leaving money on the table.

The Optimal Retry Cadence: Why Patience Pays Off

You might think hitting that retry button immediately is the best move, but it can actually backfire. Think about it: if the original decline was due to insufficient funds, an instant retry probably won’t help. It can frustrate the customer and might even get your attempts flagged as suspicious activity by their bank.

Spacing out your retries is a much smarter strategy. It gives customers breathing room to fix things on their end – maybe they need to move some money around or update their card info. A good starting point? Try 24 hours later, then again after three days, with a final attempt at the seven-day mark. This staggered approach gives the customer time while also maximizing your chances of getting paid.

Distinguishing Between Dead Ends and Temporary Hiccups

Not all payment failures are the same. A hard decline, like an expired card, requires a different approach than a soft decline – something like a temporary security block from the bank. Knowing the difference is key to effectively reducing involuntary churn. An expired card needs the customer to update their information, while a temporary block might just resolve itself.

This is where diving into your data becomes really important. Your payment processor’s logs are a goldmine of information about why declines happen. Analyzing those trends can help you tweak your retry strategy and make your communication with customers much more targeted and effective.

Seasonal Patterns and Early Warning Signs

Payment processing isn’t a constant. Things like holidays and seasonal spending habits can impact your success rates. I’ve seen payment failures jump during the holiday shopping craziness, likely due to higher card usage and those pesky temporary spending limits.

Even understanding customer behavior within your own product can give you a heads-up. A sudden drop in usage could signal potential financial issues, giving you the chance to reach out proactively before a payment even fails. For some helpful tips on delivering great service while managing costs, check out this guide: Check out our guide on providing amazing customer service on a budget.

Understanding these subtle differences helps optimize your recovery process and keep involuntary churn to a minimum. It’s not just about when you retry; it’s about how you handle the entire recovery process.

Communication That Builds Trust During Payment Issues

Let’s be honest, nobody enjoys those annoying payment failure notifications. They can feel like a digital slap on the wrist. But the most successful retention teams I’ve worked with see each dunning email as an opportunity. It’s a chance to connect with the customer on a human level and actually strengthen the relationship.

Think about it: a payment problem often puts your customer in a vulnerable spot. Responding with empathy can truly set you apart.

Finding Your Authentic Voice: Helpful, Not Pushy

Balancing brand personality with the urgency of a payment issue is tricky. You need to be clear about the payment, but avoid sounding like a collection agency. For example, ditch the harsh “Payment Failed” subject line and try something friendlier, like “Let’s get your [Product Name] subscription back on track!”.

The same principle applies to the email itself. Keep the tone conversational. Instead of corporate jargon, a simple “We noticed there might be a small hiccup with your recent payment. How can we help?” works wonders. This shows you value the customer’s overall experience, not just their money.

This is crucial because, according to TrueLayer, involuntary churn makes up 20-40% of all churn. That’s a big chunk of lost subscribers who didn’t actively choose to leave – they were locked out due to payment problems.

Multi-Channel Mastery: Knowing When and How to Communicate

Email isn’t always the best approach. Sometimes a quick SMS message is better for an urgent issue, or maybe an in-app notification if the customer is actively using your product. The trick is to use these channels strategically.

Don’t spam the same message everywhere. Adapt the message to the channel. A detailed email is fine, but an SMS should probably just offer a quick link to update payment info. For example, if a customer consistently ignores your emails, a targeted in-app message when they log in might be much more effective. This personalized approach can make a real difference.

Personalization That Matters: More Than Just a Name

Real personalization goes deeper than just using the customer’s name. Refer to their specific account activity. For example, “We noticed you’ve been actively using [Feature Name] recently. We’d hate for you to lose access!” shows you’re paying attention to their individual needs. It also reminds them of your product’s value and encourages them to fix the payment issue.

Transparency Builds Trust: Turning Challenges into Opportunities

Be honest about why the payment failed. Expired card? Insufficient funds? Clear information empowers customers to take action. It also builds trust and shows you’re not trying to hide anything.

Consider providing helpful resources like a link to their bank’s website or a guide to updating their payment info in your app. This turns a potentially negative experience into a chance to strengthen the customer relationship. Turning a potential churn situation into a positive interaction can surprisingly boost loyalty. Remember, reducing involuntary churn is as much about customer relationships as it is about recovering payments.

Calculating What Involuntary Churn Really Costs Your Business

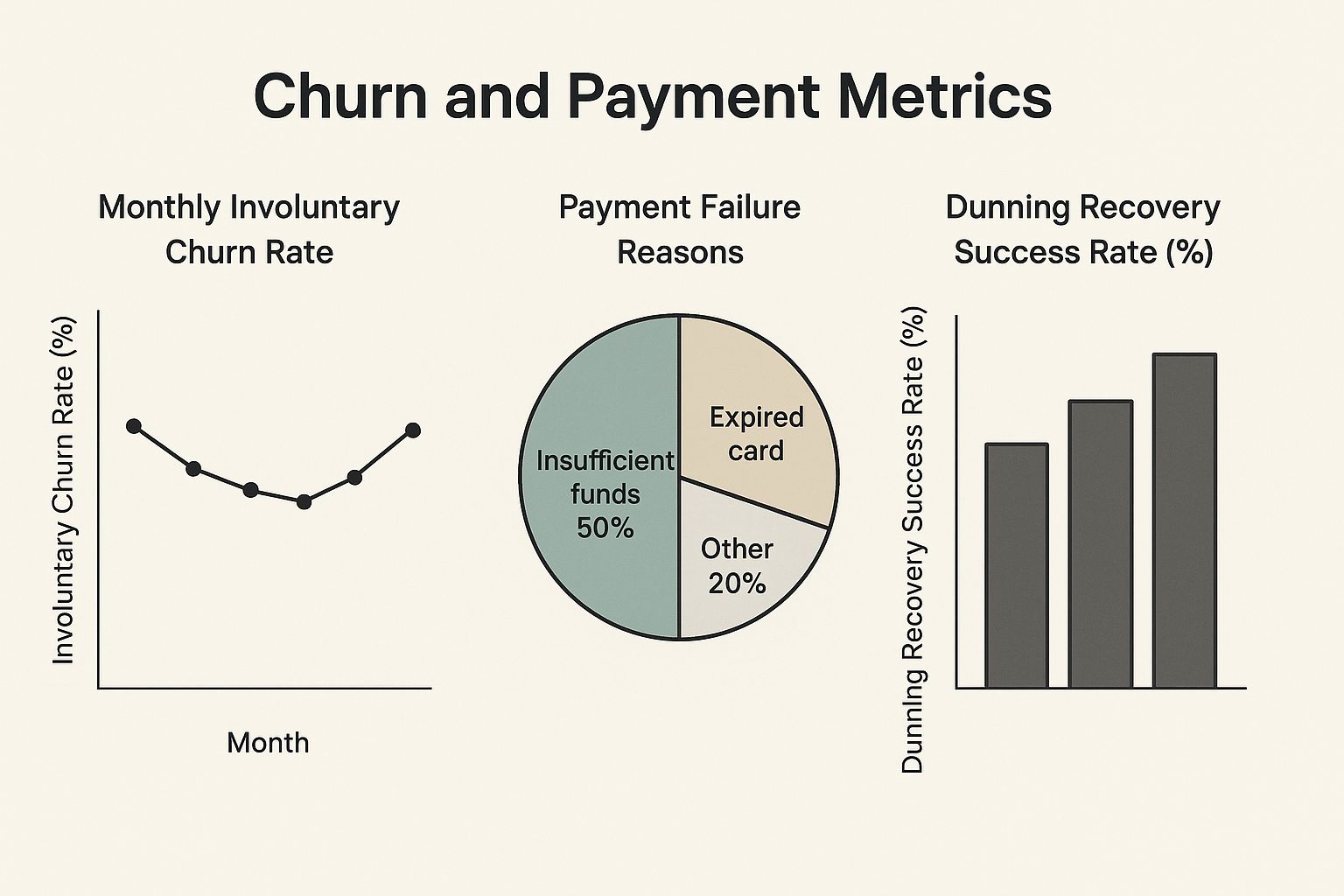

This infographic gives you a snapshot of key involuntary churn data, like monthly trends, reasons for payment failures, and how well your dunning management is working. Notice how expired cards and insufficient funds are the biggest culprits? They seriously impact your recovery rates and, ultimately, your bottom line. And it’s not just about the immediate lost subscriptions; it’s the ripple effect that really stings.

Most companies fixate on the immediate hit to Monthly Recurring Revenue (MRR), but that’s just the surface. You’ve already spent time and resources acquiring that customer. Now, you’re shelling out more cash to find a replacement, essentially paying double for the same customer spot. This messes with your Customer Lifetime Value (CLV), making each customer less profitable.

Involuntary churn also throws a wrench in expansion revenue. If a customer churns before you can upsell them or move them to a higher-tier plan, you’re losing potential growth. I once worked with a SaaS company that saw a 15% increase in average revenue per user (ARPU) just by tightening up their payment recovery system. That extra revenue can be the difference between barely making it and really flourishing. The financial impact is huge. Businesses in the U.S. lose around $136.8 billion annually due to preventable churn. That’s a wake-up call if I’ve ever heard one. For more eye-opening stats, check out these customer retention statistics.

Building a Comprehensive Cost Model

To really grasp the true cost, you need a model that sees the whole picture. This means factoring in not just the lost MRR, but also these hidden costs:

- Customer Acquisition Cost (CAC) for Replacement: Think about how much it costs to acquire a new customer to fill the gap left by the churned one.

- Reduced CLV: Calculate the potential lifetime value lost due to premature churn.

- Lost Expansion Revenue: Figure out how much potential upsell or cross-sell revenue has slipped through your fingers.

By putting numbers to these hidden costs, you build a strong argument for investing in churn reduction. And when you’re communicating with customers about payment issues, take a look at these effective email marketing examples. You might also find this helpful: Building a Customer Success Strategy to Increase Retention

To help visualize the potential return on investment, let’s look at a practical framework:

ROI Calculator for Churn Reduction Investments

This table provides a framework for calculating the return on investment from different involuntary churn reduction strategies.

| Investment Type | Implementation Cost | Expected Recovery Rate | Break-even Timeline | Annual Impact |

|---|---|---|---|---|

| Improved Dunning Emails | $500 | 5% | 3 months | $10,000 |

| Account Updater Service | $1,000 | 10% | 6 months | $25,000 |

| Smart Retry Logic | $2,000 | 15% | 9 months | $50,000 |

As you can see, even small improvements in recovery rates, driven by strategic investments, can significantly impact your annual revenue. It’s about finding the right balance between investment and potential return.

Setting Achievable Benchmarks

Once you know the costs, you can set realistic improvement goals. This means considering industry averages and your own customer segments. What’s a good recovery rate for your specific situation? Start by looking at your current performance and finding areas to improve. Even small bumps in your recovery rates can mean big revenue gains down the line. Set small, manageable goals, track how you’re doing, and tweak your strategies as you go. Don’t shoot for perfection right off the bat. Focus on getting better over time, and you’ll see the benefits add up.

Technology Stack That Actually Moves the Needle

Picking the right tools to fight involuntary churn can be a real headache. I’ve witnessed firsthand how businesses can get bogged down with overly complicated systems that end up making things worse. So, let’s ditch the jargon and focus on the tech that actually gets results. Here’s my take, based on real-world experience.

Unlocking Hidden Power: Your Payment Processor

You might be surprised by how much your payment processor can do. Many businesses only use a fraction of its potential. These platforms often have built-in intelligent retry algorithms that go way beyond basic retries. They use data to figure out the best times to retry failed payments, boosting your recovery rate without bothering your customers.

Another underutilized feature is decline analysis. Some processors use machine learning to spot patterns in failed transactions – like problems with certain banks or card types – that you’d never catch on your own. This information is incredibly valuable for fine-tuning your recovery strategy.

Streamlining the Workflow: Subscription Management Platforms

Modern subscription management platforms are a total game-changer. They integrate directly with your payment processor, letting you create powerful recovery workflows without needing to be a coding whiz or a payments expert.

These platforms can automatically send personalized emails, SMS messages, or even in-app notifications based on why and when a payment failed. This targeted, automated approach is way more effective than generic dunning emails. It’s like having a dedicated recovery team working around the clock, but without the extra cost.

Predicting the Future: Customer Data Platforms

A customer data platform (CDP) is more than just a fancy CRM. It gathers data from every customer interaction – your website, app, email marketing, and even support tickets – to create a complete picture. This allows you to identify at-risk customers before their payments fail.

Maybe they’ve stopped logging in as often, or they haven’t used your key features lately. These subtle changes in behavior can be early warning signs, giving you the chance to reach out and offer support, potentially preventing a failed payment altogether.

Behavioral Triggers: Intervening at the Right Moment

Connecting behavioral trigger systems to your CDP takes things to the next level. For example, if a customer marks a support ticket about a crucial feature as “unsolved,” this could trigger an alert for your customer success team to proactively reach out. By addressing underlying problems early, you can greatly reduce the chances of involuntary churn down the road.

Implementation Timeline and Pitfalls

Setting up these tools takes time. Integrating a payment processor with a subscription management platform could take a few weeks. A robust CDP and behavioral trigger system might take a few months. Prioritize based on your needs and resources.

One common mistake is poor integration between systems. Make sure your chosen tools work well together. Test everything thoroughly and monitor closely after launch. Track key metrics like your recovery rate, average recovery time, and customer retention rate to make sure you’re making a real impact.

Your Practical Roadmap to Sustainable Churn Reduction

So, we’ve covered the main strategies. Now let’s talk about putting them into action. Building a sustainable plan to reduce involuntary churn isn’t about magic; it’s about consistent work that pays off over time. Think of it like constructing a building – you need a solid blueprint and a steady hand.

Prioritizing Your Action Plan: Quick Wins and Long-Term Initiatives

I always suggest starting with the easy stuff. What can you do right now to make a difference? Perhaps it’s optimizing your dunning email subject lines so more people open them, or adjusting your retry schedule based on why payments usually fail. These quick wins create momentum and show early value.

Then, turn your attention to the bigger projects. Things like integrating a new subscription management platform like Zuora or implementing a customer data platform like Segment take more time and planning. Prioritize these based on their potential impact and the resources you have available. It’s a balancing act between immediate action and long-term strategy.

Getting Everyone on Board: Building Cross-Team Alignment

Lowering involuntary churn isn’t a one-person job. It needs support from everyone in the company. Customer success, finance, product development – they all have a part to play. Explain the financial impact of involuntary churn to your finance team, showing how even a small improvement means big revenue gains. Share customer feedback with your product team to highlight why a smooth payment experience is crucial.

When everyone sees how their work contributes to a shared goal, you create a powerful team against churn. To improve your payment recovery system, look into different technologies. For some practical ideas, check out these API integration examples.

Testing and Optimization: A Data-Driven Approach

Even the best plans need adjustments. A/B testing your recovery emails is a simple but effective way to figure out what works best for your customers. Experiment with different subject lines, content, and calls to action. Also, play around with your retry schedule. Does changing the timing or how often you retry improve your recovery rate?

Don’t be afraid to try things out. Data is your best friend. It shows you what’s working and what’s not, so you can constantly refine your approach. If you’re looking for more ideas on winning back lost customers, this article on How to Win Back Canceled Customers might be helpful.

Staying Ahead of the Curve: Adapting to Change

The world of payments is always changing. New rules, shifting customer expectations, and new technologies can all affect your retention rates. Stay updated on industry trends and be ready to adapt your strategies.

Keeping an eye on your key metrics – like recovery rate, average recovery time, and customer feedback – helps you spot when your efforts need a change. Being proactive like this keeps you ahead of potential problems and makes sure your churn reduction efforts keep working in the long run. Remember, this isn’t a set-it-and-forget-it type of deal. Regular monitoring and adjustments are the keys to long-term success.

Ready to revamp your payment recovery and significantly reduce involuntary churn? Stunning provides a simple, automated solution that works with your existing Stripe or Subbly setup. Start your free 15-day trial with Stunning today and reclaim lost revenue!